- TOPLEY'S TOP 10

- Posts

- SMARTER IN 10

SMARTER IN 10

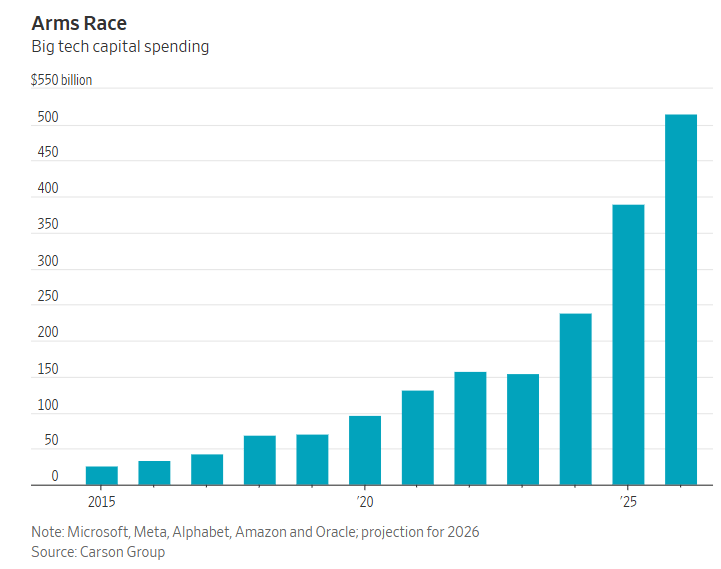

Big Tech Capital Spending on AI Build Out

?

1. Big Tech Capital Spending on AI Build Out

WSJ

?

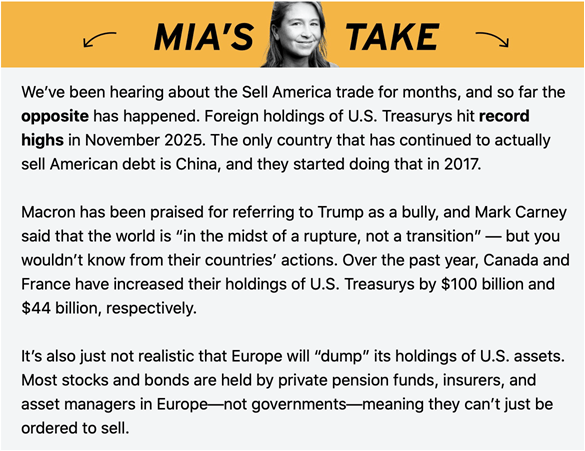

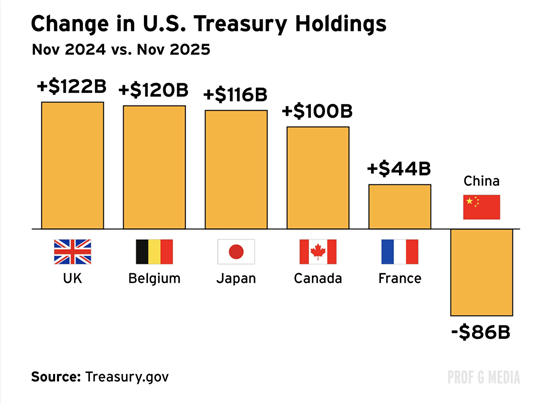

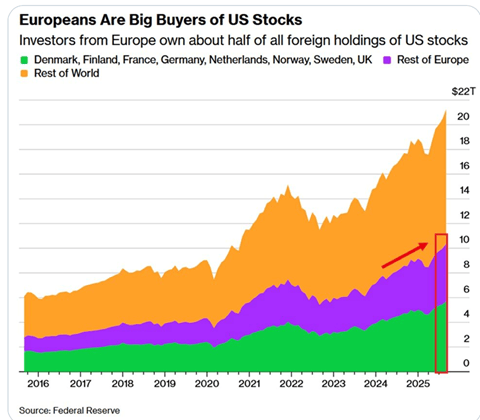

2. Sell America Not Showing Up in Money Flows

Prof G Markets

…

3. Sell America Not Showing Up in Money Flows

Barrons-Healthy capital inflows into U.S. capital markets, which totaled some $1.569 trillion in the 12 months through November, according to the latest Treasury International Capital Data. That included $481 billion going into Treasury notes and bonds and government agency securities.

But while market watchers tend to concentrate on foreign purchases of Treasuries as an indication of global support for Uncle Sam’s borrowing needs, the biggest international inflows of the past 12 month were into U.S. equities. Not surprisingly, the world was coming to America to participate in the artificial-intelligence boom, buying $689 billion of U.S. equities, or 44% of long-term securities purchases, in the span. Foreign purchases of corporate bonds (an increasing amount of which funds AI buildouts) accounted for a quarter of long-term securities purchases. So, AI is not only an essential factor in the stock market’s advance but also a key component in funding the U.S. current-account deficit.

Barron’s

…

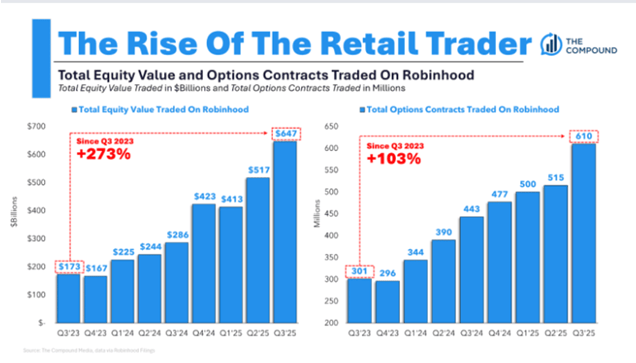

4. The Rise of Retail Trader

Irrelevant Investor Blog

…

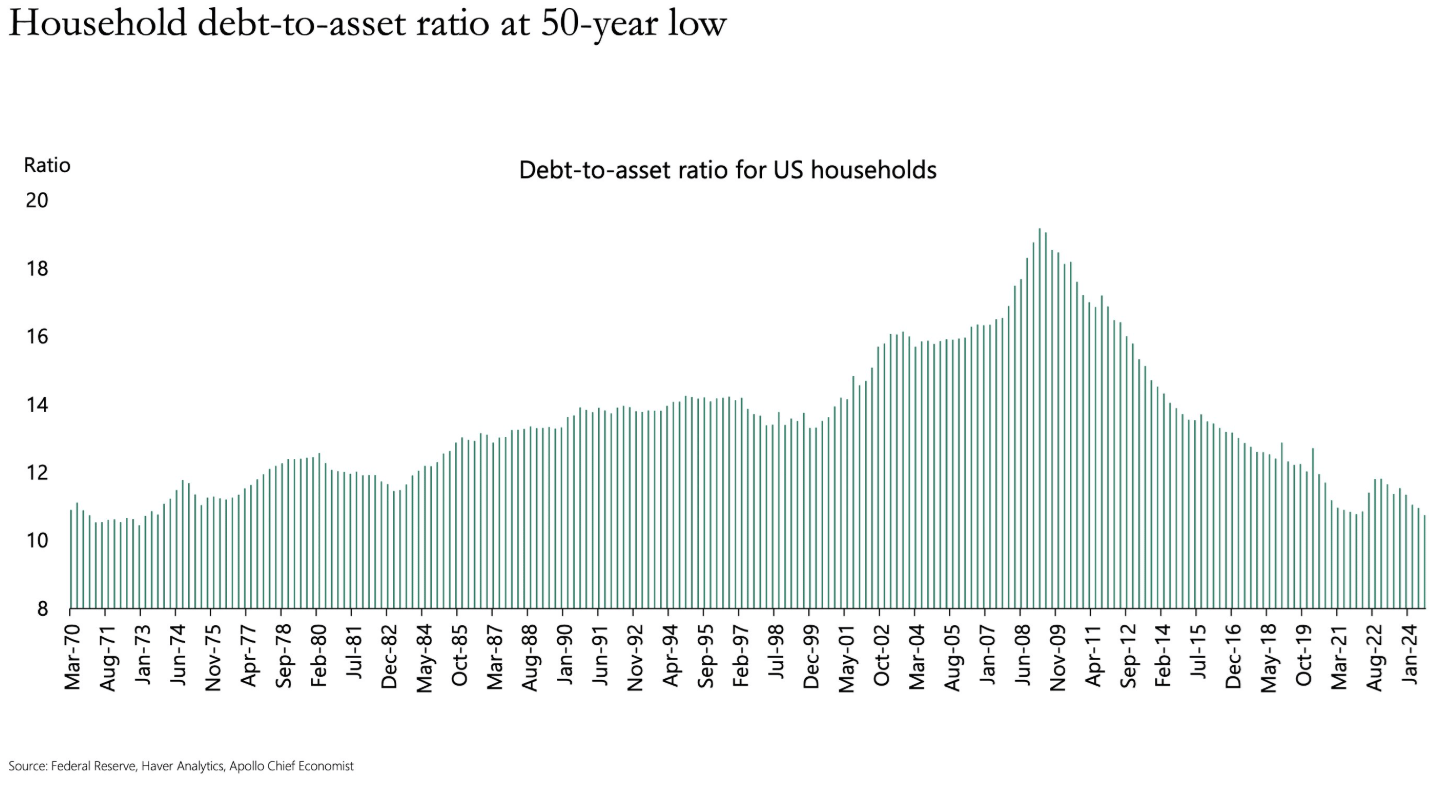

5. Household Debt to Asset Ratio at 50-Year Low

Apollo Academy

…

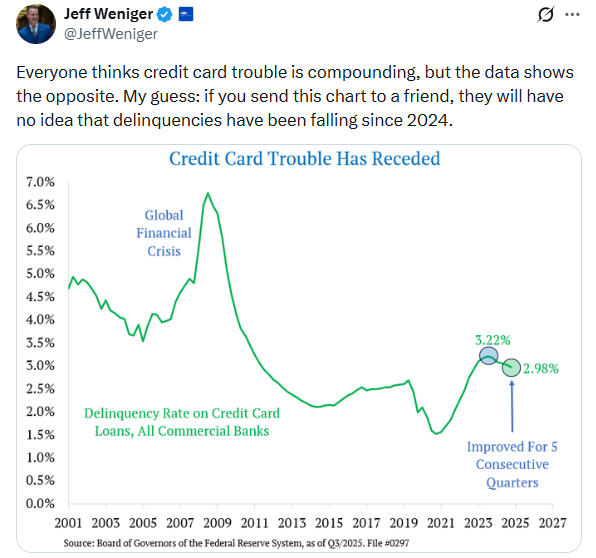

6. Credit Card Debt Delinquencies are Receding

@JeffWeniger

?

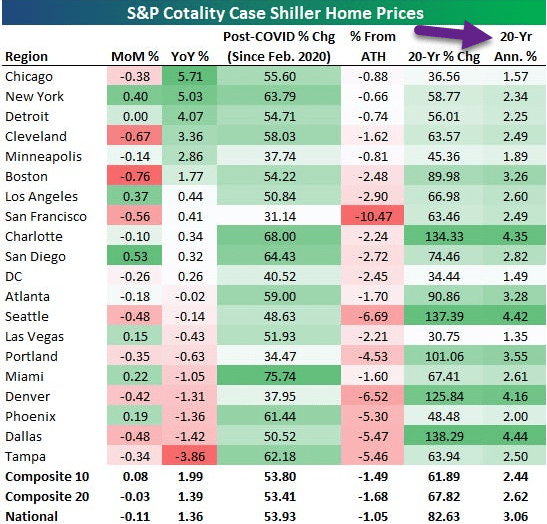

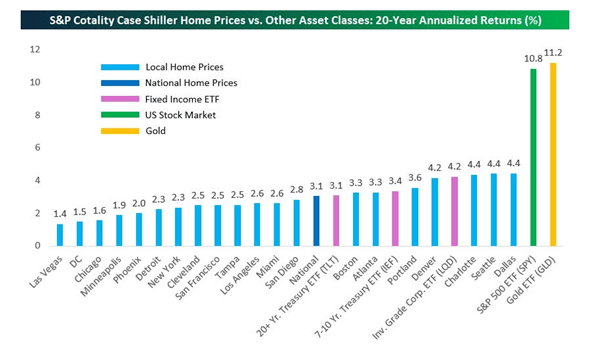

7. Home Ownership-A Place to Live Not an Investment

Bespoke Investment Group-As shown below, most cities tracked have seen annualized home price gains of less than 3% over the last twenty years. That’s worse than the 3.1% annualized return for the long-term Treasury ETF (TLT).

Bespoke Investment Group

?

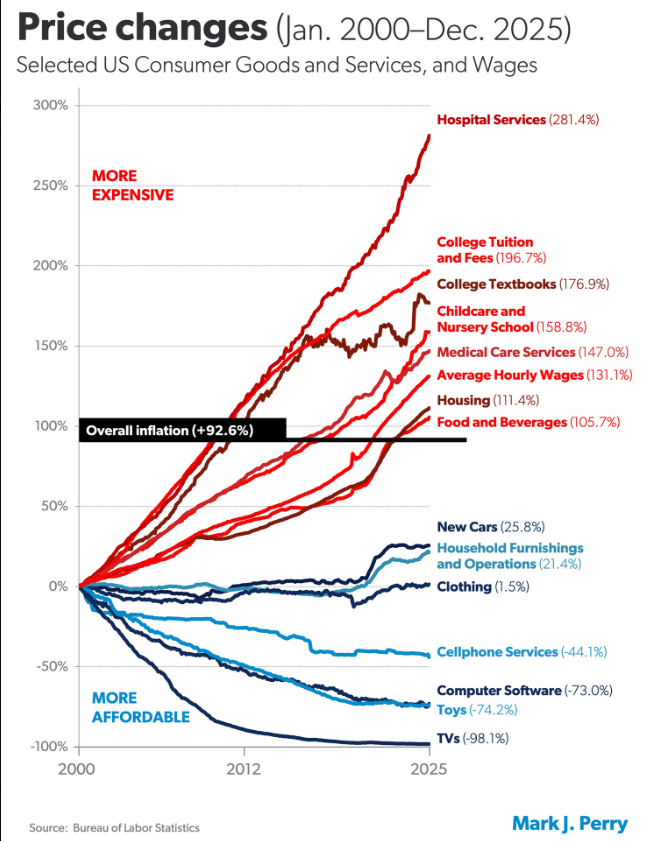

8. Price Changes 25 Years

@HeresyFinancial

…»>

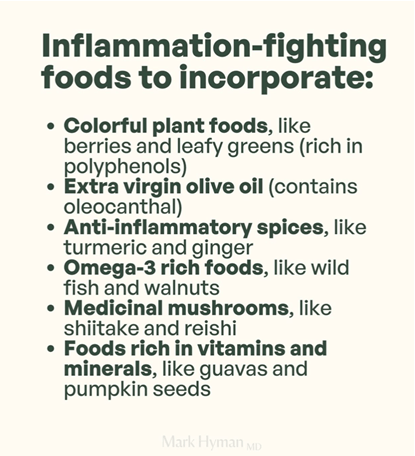

9. #1 Cause of Disease Inflammation -Dr.Hyman

Dr. Mark Hyman

»>…

10. I've been investing for 45 years: 5 dumb mistakes nearly every investor makes

by Stacy Johnson CPA

Our team of professional journalists has more than 100 years of combined experience writing articles like this. Help us continue producing award-winning content by clicking the follow button above.

I bought my first stock more than 45 years ago. Since then, I’ve lived through the crash of 1987 (Black Monday), the dot-com bubble, the Great Recession, and the post-pandemic inflation spike.

Market cycles change, but one thing never does: human nature.

In my four decades of watching people try to build wealth, I have noticed that the biggest threat to your portfolio is rarely the Federal Reserve, the President, or the price of oil. It is the person staring back at you in the mirror.

We’re all hardwired to make bad financial decisions. We run from pain (selling when the market drops) and chase pleasure (buying when the market soars).

If you want to retire rich, you have to stop acting like a human and start acting like an investor. Here are five things to avoid.

1. Trying to time the market

This is the classic ego trap. You convince yourself you can get out before the crash and get back in before the rebound. Let me be clear: You can’t. Even the professionals can’t.

When you try to time the market, you have to be right twice. You have to sell at the top and buy at the bottom. If you miss by just a few days, you destroy your returns.

According to data from J.P. Morgan, if you stayed fully invested in the S&P 500 from 2005 to 2024, you earned an annualized return of roughly 10%. But if you tried to get cute and missed just the 10 best days in that 20-year period, your return drops to a bit over 6%.

Think about that. Missing two weeks of action over two decades cut your gains almost in half. The market’s biggest jumps often happen right after its biggest drops. If you are freaking out about the stock market and waiting for the “dust to settle,” you have already lost.

2. Paying high fees because you aren’t paying attention

In every other area of life, you get what you pay for. A Ferrari costs more than a Ford because it’s faster and presumably better made. You get something for your money. In investing, the opposite is often true. You can pay more for the same, or even worse, performance.

It’s just this simple: The more you pay in fees, the less you keep.

3. Thinking you can pick winning stocks

I’m a believer in buying individual stocks. The reason is simple: I’ve made a ton of money over the years doing it.

I’ve owned stock in Apple, Microsoft, Amazon, Nvidia, Google and other big winners for many years; in the case of Apple, 25 years. Of course, I’ve also had losers along the way, but I’ve definitely beaten the returns I would have gotten from a broad-based S&P Index fund or ETF.

But here’s the thing: I spent 10 years as an investment advisor and for decades I’ve spent several hours every weekday reading about this stuff. Every weeknight I watch a couple of CNBC shows for tips and information.

Sound like you? If it doesn’t, don’t buy individual stocks.

The data shows how statistically unlikely you are to beat the market over the long run by picking individual stocks. Consider this: over a 15-year period, nearly 90% of active large-cap fund managers fail to beat the S&P 500. And the managers of these actively-managed funds are professional investors, with institutional research and every bell and whistle at their fingertips.

If they can’t beat the index, what makes you think you can?

Unless you’re willing to invest a lot of time into research, stop trying to find the needle in the haystack and just buy the haystack.

As I cover in the golden rules of becoming a millionaire, a low-cost S&P 500 index fund will outperform the vast majority of stock pickers over a lifetime.

4. Letting your emotions drive the bus

When the market tanks, your brain screams “Sell!” to stop the pain. When your neighbor brags about making a killing in crypto, your brain screams “Buy!” to avoid missing out.

This emotional whiplash is expensive. The research firm Dalbar publishes an annual “Quantitative Analysis of Investor Behavior” (QAIB) report, and the results are always depressing.

In 2024, the S&P 500 returned a massive 25.02%. But the average equity fund investor? They only earned 16.54%.

That is a gap of nearly 8.5 percentage points. Why? Because investors panicked, sold at the wrong times, or chased trends that had already peaked. The market did its job. The investors didn’t.

Here’s something I’ve learned over the years. If you lay awake at night staring at the ceiling because you’re worried about your stocks, you have too much invested in stocks. That’s going to cause you to make mistakes.

5. Focusing on the rear-view mirror

There is a cognitive bias called “recency bias.” It means we give more weight to what happened recently than what happened further in the past.

If tech stocks soared last year, we dump all our money into tech. If bonds crashed, we sell all our bonds. We chase past performance, assuming it will continue forever. It rarely does.

Winners rotate. The hot sector of 2025 might be the dog of 2026. If you constantly chase what just worked, you are buying high and selling low—the exact opposite of how you build real wealth.

Stick to a diversified plan. Rebalance when things get out of whack. And for heaven’s sake, stop looking at your account balance every day.

How savvy investors double their retirement savings (Sponsored)

A Vanguard study found that, on average, a hypothetical $500,000 investment over 25 years would grow to $1.7 million if you manage it yourself, but more than $3.4 million if you work with a financial adviser. That’s twice as much!

If you’ve got $100,000 in investible assets, you qualify for a free appointment with a vetted financial advisor in your area.

»>…

Did someone forward this email to you? Get your own:

Disclosure

Indices that may be included herein are unmanaged indices and one cannot directly invest in an index. Index returns do not reflect the impact of any management fees, transaction costs or expenses. The index information included herein is for illustrative purposes only.

Material for market review represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results.

Material compiled by Lansing Street Advisors is based on publicly available data at the time of compilation. Lansing Street Advisors makes no warranties or representation of any kind relating to the accuracy, completeness or timeliness of the data and shall not have liability for any damages of any kind relating to the use such data.

To the extent that content includes references to securities, those references do not constitute an offer or solicitation to buy, sell or hold such security as information is provided for educational purposes only. Articles should not be considered investment advice and the information contain within should not be relied upon in assessing whether or not to invest in any securities or asset classes mentioned. Articles have been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Securities discussed may not be suitable for all investors. Please keep in mind that a company’s past financial performance, including the performance of its share price, does not guarantee future results.

Lansing Street Advisors is a registered investment adviser with the State of Pennsylvania.